Read this text on the budgeting process and tax policy in the United States. What is the difference between progressive and regressive tax policies? What are the potential benefits and drawbacks of progressive and regressive taxation?

A country spends, raises, and regulates money in accordance with its values. In all, the federal government's budget for 2020 was $6.55 trillion. This chapter has provided a brief overview of some of the budget's key areas of expenditure and, thus, some insight into modern American values. But these values are only part of the budgeting story. Policymakers make considerable efforts to ensure that long-term priorities are protected from the heat of the election cycle and short-term changes in public opinion. The decision to put some policymaking functions out of the reach of Congress also reflects economic philosophies about the best ways to grow, stimulate, and maintain the economy. The role of politics in drafting the annual budget is indeed large, but we should not underestimate the challenges elected officials face as a result of decisions made in the past.

Until the 1930s, most policy advocates argued that the best way for the government to interact with the economy was through a hands-off approach formally known as laissez-faire economics. These policymakers believed the key to economic growth and development was the government's allowing private markets to operate efficiently. Proponents of this school of thought believed private investors were better equipped than governments to figure out which sectors of the economy were most likely to grow and which new products were most likely to be successful. They also tended to oppose government efforts to establish quality controls or health and safety standards, believing consumers themselves would punish bad behavior by not trading with poor corporate citizens. Finally, laissez-faire proponents felt that keeping the government out of the business of business would create an automatic cycle of economic growth and contraction. Contraction phases in which there is no economic growth for two consecutive quarters, called recessions, would bring business failures and higher unemployment. But this condition, they believed, would correct itself on its own if the government simply allowed the system to operate.

The Great Depression challenged the laissez-faire view, however. When President Franklin Roosevelt came to office in 1933, the United States had already been in the depths of the Great Depression for several years since the stock market crash of 1929. Roosevelt sought to implement a new approach to economic regulation known as Keynesianism. Named for its developer, the economist John Maynard Keynes, Keynesian economics argues that it is possible for a recession to become so deep and last for so long that the typical models of economic collapse and recovery may not work. Keynes suggested that economic growth was closely tied to the ability of individuals to consume goods. It didn't matter how or where investors wanted to invest their money if no one could afford to buy the products they wanted to make. And in periods of extremely high unemployment, wages for newly hired labor would be so low that new workers would be unable to afford the products they produced.

Keynesianism counters this problem by increasing government spending in ways that improve consumption. Some of the proposals Keynes suggested were payments or pensions for the unemployed and retired, as well as tax incentives to encourage consumption in the middle class. His reasoning was that these individuals would be most likely to spend the money they received by purchasing more goods, which in turn would encourage production and investment. Keynes argued that the wealthy class of producers and employers had sufficient capital to meet the increased demand of consumers that government incentives would stimulate. Once consumption had increased and capital was flowing again, the government would reduce or eliminate its economic stimulus, and any money it had borrowed to create it could be repaid from higher tax revenues.

Keynesianism dominated U.S. fiscal or spending policy from the 1930s to the 1970s. By the 1970s, however, high inflation began to slow economic growth. There were a number of reasons, including higher oil prices and the costs of fighting the Vietnam War. However, some economists, such as Arthur Laffer, began to argue that the social welfare and high tax policies created in the name of Keynesianism were overstimulating the economy, creating a situation in which demand for products had outstripped investors' willingness to increase production. They called for an approach known as supply-side economics, which argues that economic growth is largely a function of the productive capacity of a country. Supply-siders have argued that increased regulation and higher taxes reduce the incentive to invest new money into the economy to the point where little growth can occur. They have advocated reducing taxes and regulations to spur economic growth.

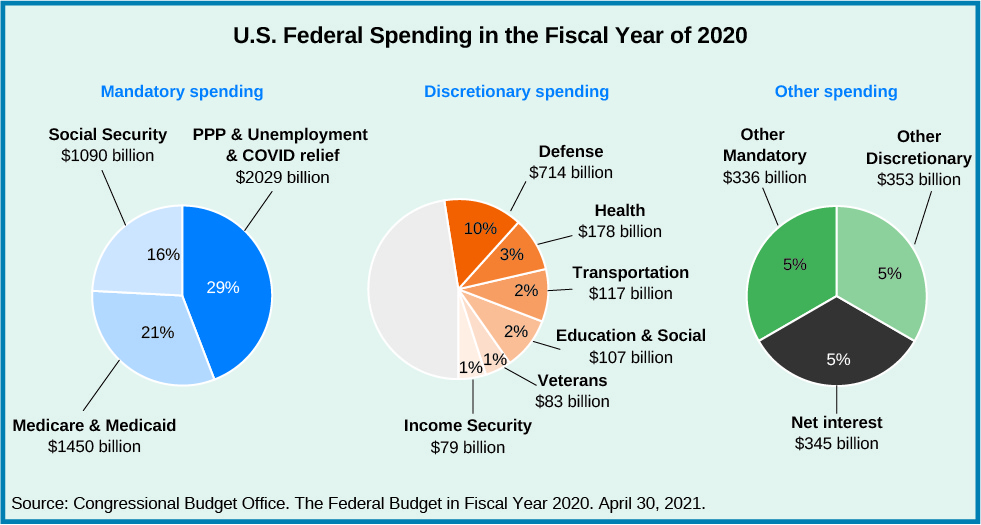

The desire of Keynesians to create a minimal level of aggregate demand, coupled with a Depression-era preference to promote social welfare policy, led the president and Congress to develop a federal budget with spending divided into two broad categories: mandatory and discretionary (see Figure 16.15). Of these, mandatory spending is the larger, consisting of about $4.9 trillion of the 2020 budget, or roughly 71 percent of all federal expenditures.

The overwhelming portion of mandatory spending is earmarked for entitlement programs guaranteed to those who meet certain qualifications, usually based on age, income, or disability. These programs, discussed above, include Medicare and Medicaid, Social Security, and major income security programs such as unemployment insurance and SNAP. The costs of programs tied to age are relatively easy to estimate and grow largely as a function of the aging of the population. Income and disability payments are a bit more difficult to estimate. They tend to go down during periods of economic recovery and rise when the economy begins to slow down, in precisely the way Keynes suggested. A comparatively small piece of the mandatory spending pie, about 14 percent, is devoted to benefits designated for former federal employees, including military retirement and many Veterans Administration programs.

Figure 16.15 This chart of U.S. federal spending for 2020 shows the proportions of mandatory and discretionary spending, about 66 percent and 19 percent, respectively.

Figure 16.16 The war in Afghanistan, ongoing since 2001, has cost the United States billions of dollars in discretionary military spending authorized by Congress every year. In early 2021, President Joe Biden announced plans to fully withdraw U.S. troops from Afghanistan by September 11, 2021, the twentieth anniversary of the 9/11 attacks.

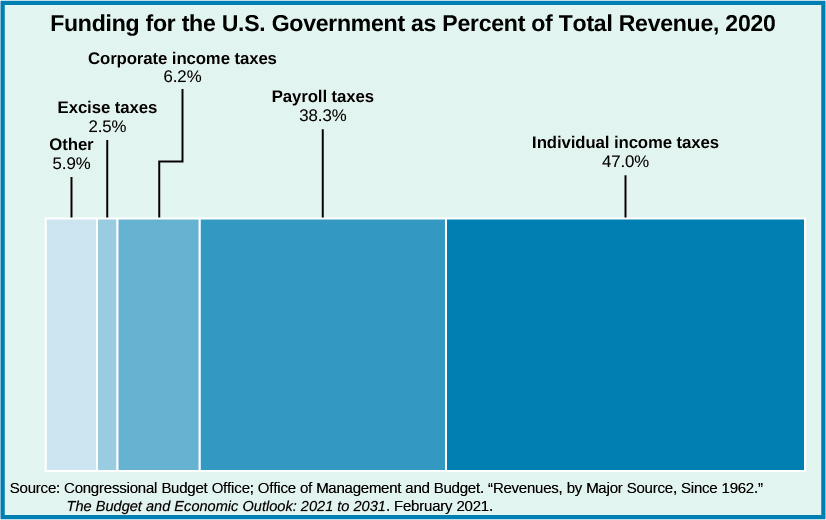

The other option available for balancing the budget is to increase revenue. All governments must raise revenue in order to operate. The most common way is by applying some sort of tax on residents (or on their behaviors) in exchange for the benefits the government provides (Figure 16.17). However, as necessary as taxes are, they are not without potential downfalls. First, the more money the government collects to cover its costs, the less residents are left with to spend and invest. Second, attempts to raise revenues through taxation may alter the behavior of residents in ways that are counterproductive to the state and the broader economy. Excessively taxing necessary and desirable behaviors like consumption (with a sales tax) or investment (with a capital gains tax) will discourage citizens from engaging in them, potentially slowing economic growth. The goal of tax policy, then, is to determine the most effective way of meeting the nation's revenue obligations without harming other public policy goals.

Figure 16.17 A U.S. marine fills out an income tax form. Income taxes in the United States are progressive taxes.

Figure 16.18 A gas station shows fuel prices over $3.00 a gallon in 2005, shortly after Hurricane Katrina disrupted gas production in the Gulf of Mexico. Taxes on gasoline that are based on the quantity purchased are regressive taxes.

Figure 16.19 The taxes tied to individuals, not businesses, overwhelmingly fund the government.

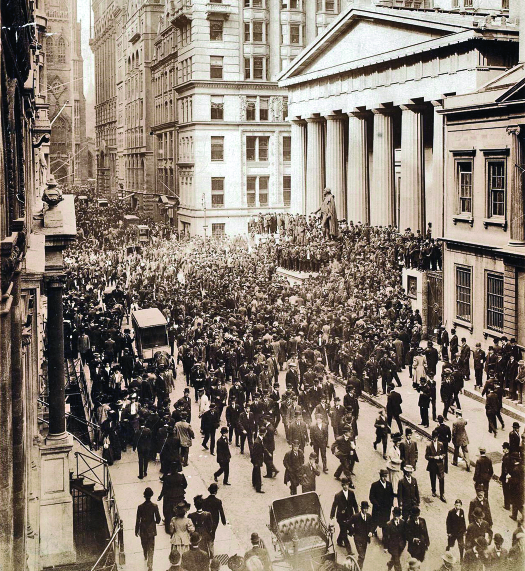

Financial panics arise when too many people, worried about the solvency of their investments, try to withdraw their money at the same time. Such panics plagued U.S. banks until 1913 (Figure 16.20) when Congress enacted the Federal Reserve Act. The act established the Federal Reserve System, also known as the Fed, as the central bank of the United States. The Fed's three original goals to promote were maximum employment, stable prices, and moderate long-term interest rates. All of these goals bring stability. The Fed's role is now broader and includes influencing monetary policy (the means by which the nation controls the size and growth of the money supply), supervising and regulating banks, and providing them with financial services like loans.

Figure 16.20 Investors crowd Wall Street during the Bankers Panic of 1907.

If you have read or watched the news for the past several years, perhaps you have heard the names Janet Yellen, Ben Bernanke, or Alan Greenspan. Bernanke, Greenspan, and Yellen (Figure 16.21) are all recent past chairs of the board of governors of the Federal Reserve System; Jerome Powell is the current chair. The role of the Fed chair is one of the most important in the country. By raising or lowering banks' interest rates, the chair has the ability reduce inflation or stimulate growth. The Fed's dual mandate is to keep inflation low (under 2 percent) and unemployment low (below 5 percent), but efforts to meet these goals can often lead to contradictory monetary policies.

Figure 16.21 Economist Alan Greenspan (a) was chair of the board of governors of the Federal Reserve System from 1987 to 2006, the second-longest tenure of any chair. Janet Yellen (b) succeeded Ben Bernanke as chair in 2014, after serving as vice chair for four years. Prior to serving on the Federal Reserve Board, Yellen was president and CEO of the Federal Reserve Bank of San Francisco. She was succeeded by Jerome Powell in February 2018 and has been serving as secretary of the Treasury since January 2021.

The Fed, and by extension its chair, have a tremendous responsibility. Many of the economic events of the past five decades, both good and bad, are the results of Fed policies. In the 1970s, double-digit inflation brought the economy almost to a halt, but when Paul Volcker became chair in 1979, he raised interest rates and jump-started the economy. After the stock market crash of 1987, then-chair Alan Greenspan declared, "The Federal Reserve, consistent with its responsibilities as the nation's central bank, affirmed today its readiness to…support the economic and financial system." His lowering of interest rates led to an unprecedented decade of economic growth through the 1990s. In the 2000s, consistently low interest rates and readily available credit contributed to the sub-prime mortgage boom and subsequent bust, which led to a global economic recession beginning in 2008.

Should the important tasks of the Fed continue to be pursued by unelected appointees like those profiled in this box, or should elected leaders be given the job? Why?

Source: OpenStax, https://openstax.org/books/american-government-3e/pages/16-5-budgeting-and-tax-policy

This work is licensed under a Creative Commons Attribution 4.0 License.

This work is licensed under a Creative Commons Attribution 4.0 License.